HS codes, customs duties and import taxes are closely connected when commercial goods enter Canada. The HS code identifies the product for tariff purposes, the country of origin determines the tariff treatment, and the value for duty provides the base for calculating customs charges. If any of these elements is incorrect, the importer may face reassessment, clearance delays, penalties, storage charges or an inaccurate landed cost.

This guide explains how the Canadian tariff classification system works, how import duty and GST are calculated, which documents support classification, and what Canadian businesses should check before shipping goods from China. TopShipping works as a freight forwarder from China to Canada, coordinating supplier pickup, freight, customs documentation and final delivery for commercial shipments.

HS Code, Duty and Tax Requirements at a Glance

| Import element | What it determines | What the importer should verify |

|---|---|---|

| 10-digit Canadian tariff classification | Product classification, regular customs duty rate and statistical reporting | Product identity, material, function, technical specifications and level of manufacture |

| Country of origin | Applicable tariff treatment, preferential treatment and possible trade measures | Where the goods were manufactured or substantially transformed, not only where they were shipped from |

| Value for duty | Base amount used to calculate customs duty | Transaction value, currency conversion and any additions or deductions required by customs valuation rules |

| GST and other import taxes | Tax payable at importation | Duty-paid value, exemptions, excise charges and product-specific tax rules |

| Trade remedies or surtaxes | Additional charges beyond the regular tariff rate | Whether the product, origin, exporter or manufacturer is covered by a current measure |

| Importer registration | Ability to account for commercial imports and pay amounts owing | Business Number, import-export program account and CARM access |

What Is an HS Code in Canada?

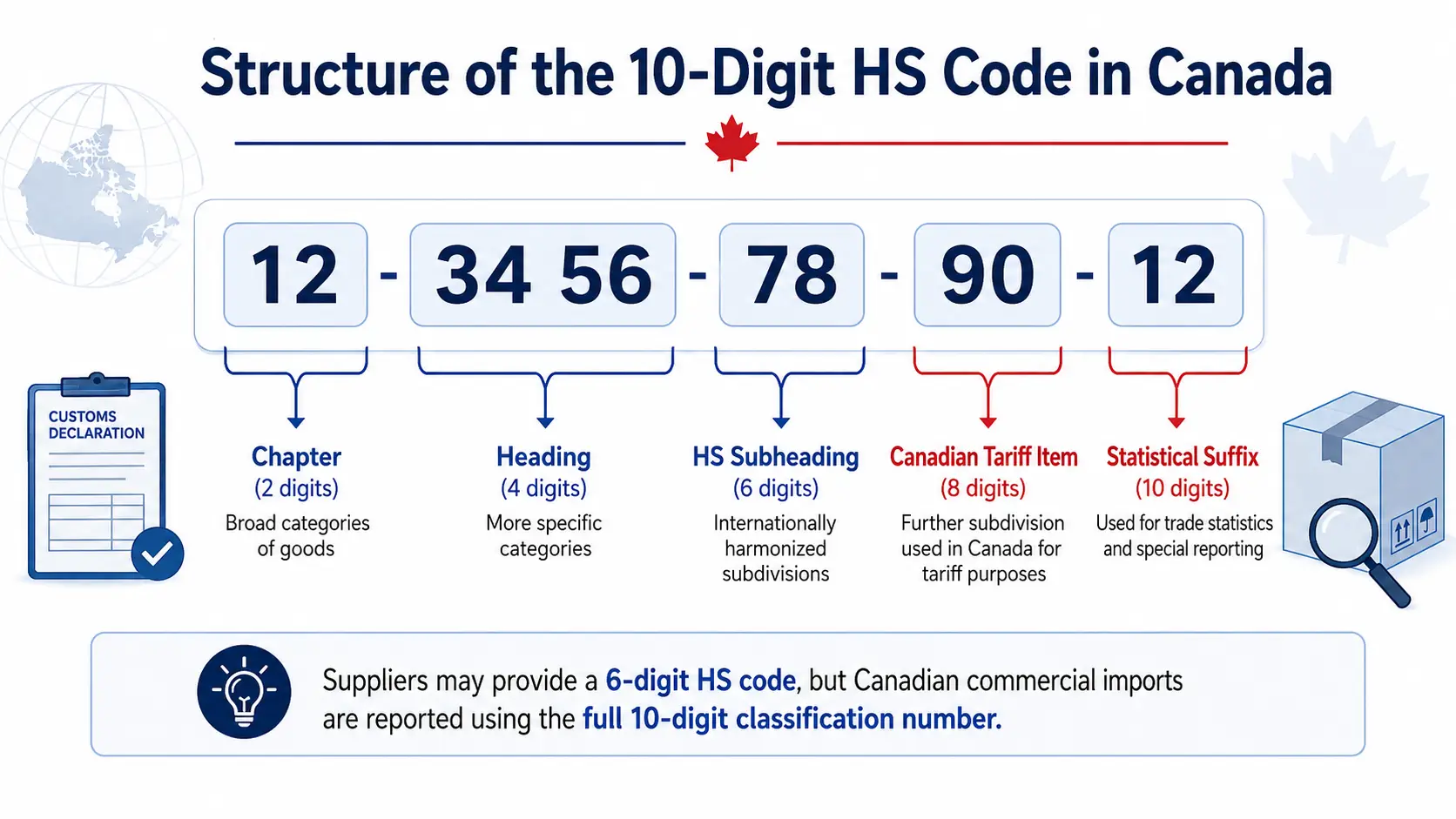

HS stands for Harmonized System. It is the international product nomenclature used to organize traded goods into sections, chapters, headings and subheadings. Canadian importers often search for an “HS code,” but the number required to report commercial goods to the Canada Border Services Agency is the complete 10-digit Canadian tariff classification number.

The first six digits follow the international HS structure. Canada adds four more digits to identify the Canadian tariff item and statistical suffix. This means a six-digit code from a Chinese supplier can be a useful starting point, but it is not automatically the complete code required for a Canadian customs declaration.

How the 10-Digit Canadian Classification Number Is Structured

| Digits | Classification level | Purpose |

|---|---|---|

| 1–2 | Chapter | Broad product family |

| 1–4 | Heading | More specific category within the chapter |

| 1–6 | HS subheading | Internationally harmonized classification level |

| 7–8 | Canadian tariff item | Level at which the Canadian customs duty rate is assigned |

| 9–10 | Canadian statistical suffix | Additional reporting detail required for Canadian imports |

All ten digits should be confirmed against the current 2026 Canadian Customs Tariff. An old classification spreadsheet, a supplier invoice or a code used in another country should not be treated as the final authority.

Why the Correct HS Code Matters

The tariff classification affects more than the regular duty percentage. It can determine whether the goods are duty-free, whether a permit or certificate is required, whether anti-dumping or countervailing duties may apply, and whether the shipment is subject to marking, labelling, safety or other regulatory controls.

An incorrect code can produce several different problems:

- Underpayment or overpayment of customs duty

- CBSA reassessment after release

- Administrative monetary penalties or interest

- Delays while product details are reviewed

- Incorrect application of a tariff treatment

- Failure to identify a surtax or trade-remedy measure

- Inconsistent records across invoices, customs entries and accounting systems

The importer of record remains responsible for the accuracy of the declaration even when a supplier, freight forwarder or customs broker assists with the shipment.

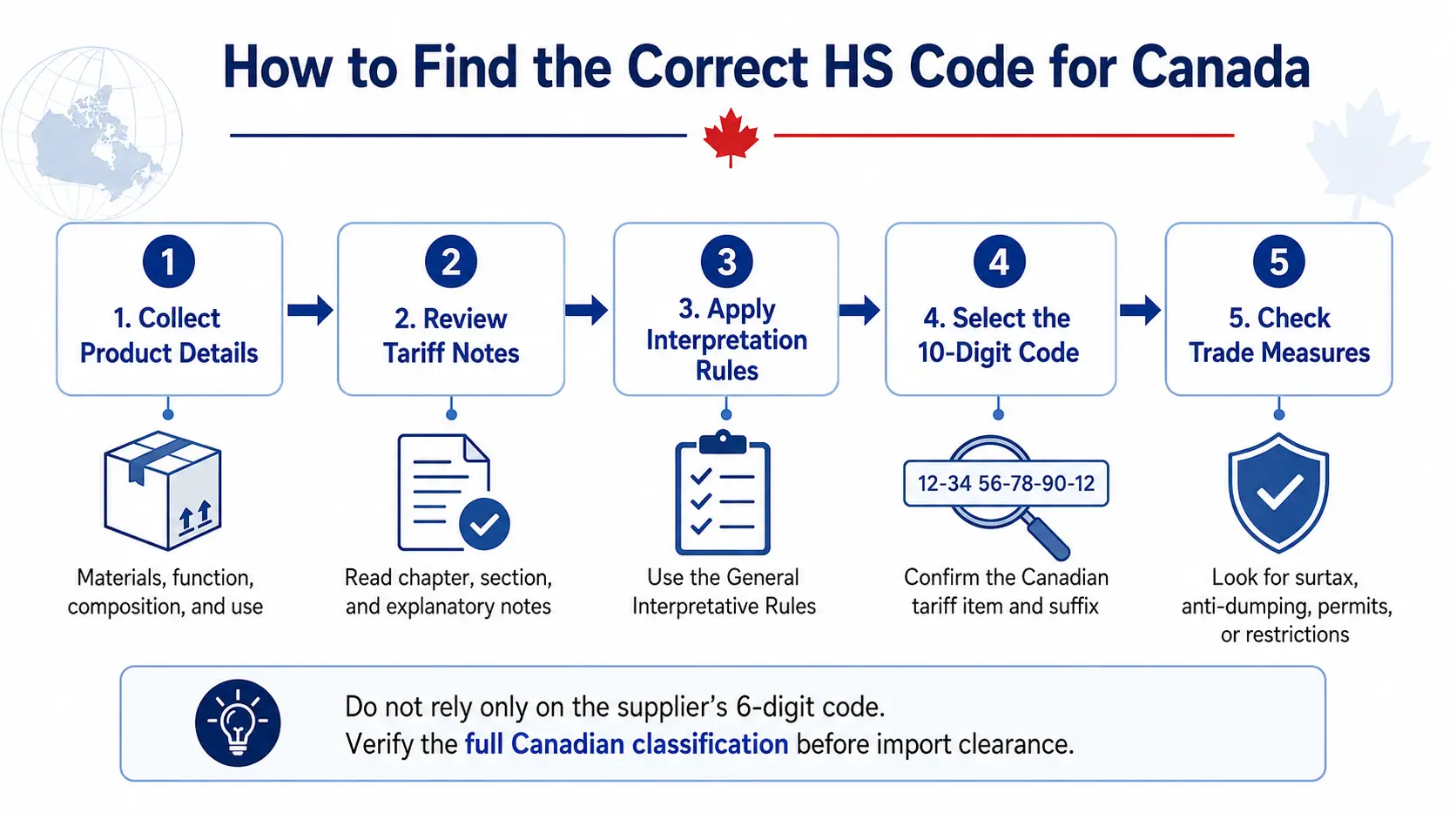

How to Find the Correct HS Code for Canada

Tariff classification should be based on the characteristics of the goods as imported. Marketing names and short supplier descriptions are often insufficient because similar-looking products can fall under different headings depending on their material, principal function, construction or intended use.

1. Collect Complete Product Information

Before searching the tariff, prepare enough technical information to distinguish the product from similar goods:

- Commercial and technical product name

- Main function and normal use

- Material composition and percentage by material where relevant

- Dimensions, capacity, power, voltage or performance specifications

- Whether the item is complete, unfinished, assembled or unassembled

- Whether it is a machine, part, accessory, set or composite good

- Model number, SKU, catalogue, drawings and product photographs

- Battery, chemical, food-contact, medical or wireless features

- Manufacturing process when it affects classification

2. Review Section Notes, Chapter Notes and Heading Wording

Classification is not based only on keyword matching. The legal wording of headings, section notes and chapter notes can include or exclude products. A code that appears correct from a simple product-name search may be wrong after the relevant legal notes are applied.

3. Apply the General Rules for the Interpretation of the Harmonized System

The General Interpretative Rules establish the sequence used to classify incomplete goods, mixtures, composite products, sets and goods that could appear to fit more than one heading. For technical products, the essential character, principal function or most specific description may be decisive.

4. Select the Full Canadian Tariff Item and Statistical Suffix

After identifying the six-digit subheading, continue through the Canadian tariff schedule to the correct eight-digit tariff item and ten-digit classification number. The duty rate is assigned at the tariff-item level, while the complete ten-digit number is required for reporting.

5. Check Current Measures and Keep a Classification Record

Record the product specifications, tariff references and reasoning used to support the classification. For high-value, recurring or technically ambiguous goods, an importer may request a binding advance ruling from the CBSA rather than relying only on an informal opinion.

Can You Use the HS Code Provided by a Chinese Supplier?

A supplier’s code should be treated as reference information, not as automatic confirmation of the Canadian classification. China and Canada both use the international six-digit HS framework, but their national tariff extensions, statistical codes and administrative interpretations can differ.

| Supplier information | How it should be used in Canada |

|---|---|

| Six-digit HS subheading | Useful starting point, but the product details and Canadian tariff notes must still be reviewed |

| Chinese 8-digit, 10-digit or longer customs code | Do not copy directly into the Canadian declaration; national extensions are country-specific |

| Code used for a previous shipment | Verify that the product specifications and current tariff schedule are unchanged |

| Generic code used for “parts” or “accessories” | Review carefully because parts provisions often depend on the machine, material and specific function |

| Code selected only to obtain a lower duty rate | Reject unless the legal classification can be supported by the goods and tariff rules |

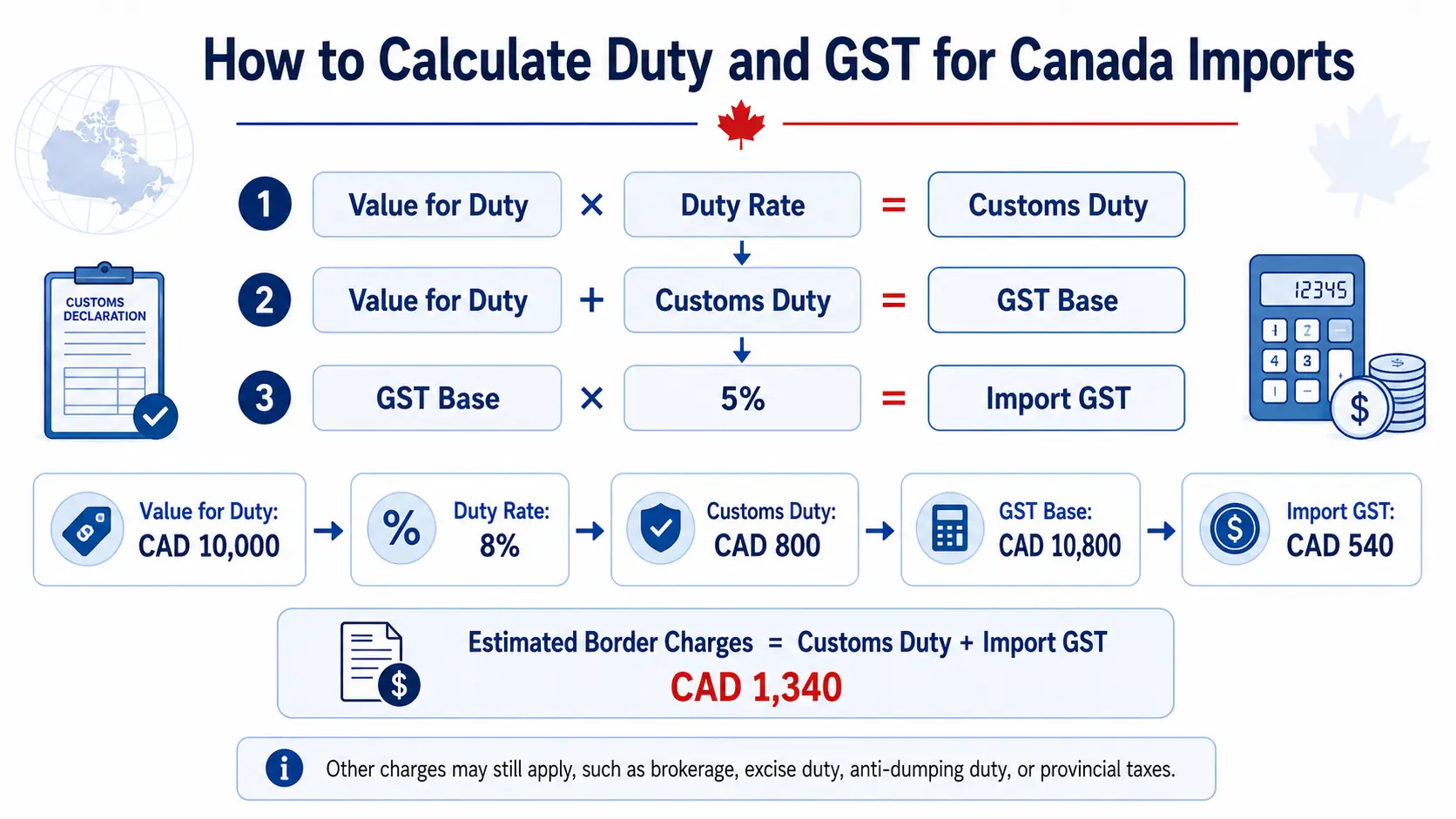

How Are Import Duties Calculated in Canada?

The regular customs duty is generally calculated by multiplying the established value for duty in Canadian dollars by the applicable customs duty rate. The rate is found under the correct Canadian tariff item and tariff treatment.

Customs duty = Value for duty × Applicable duty rate

The result can still be affected by preferential tariff treatment, remission orders, tariff-rate quotas, surtaxes, anti-dumping duties, countervailing duties or other product-specific measures. A “Free” regular tariff rate does not necessarily mean the shipment will have no customs-related charges.

Simplified Duty and GST Example

Assume the customs value has already been established at CAD 20,000, the regular duty rate is 7%, and no excise duty or additional trade measure applies:

| Calculation | Amount |

|---|---|

| Value for duty | CAD 20,000.00 |

| Customs duty: CAD 20,000 × 7% | CAD 1,400.00 |

| GST base: CAD 20,000 + CAD 1,400 | CAD 21,400.00 |

| GST: CAD 21,400 × 5% | CAD 1,070.00 |

| Total customs duty and GST | CAD 2,470.00 |

This is a planning example only. It excludes brokerage, disbursement, inspection, storage, terminal handling, freight and final delivery charges. It also assumes that the value for duty, duty rate and tax treatment have already been correctly determined.

GST, HST and Other Taxes on Imported Goods

Most commercial goods imported into Canada are subject to 5% federal GST at the time of importation. For a standard calculation, GST is assessed on the duty-paid value, which generally includes the value for duty plus customs duty and applicable excise amounts.

Importers should not simply apply the retail HST rate of the destination province to every commercial customs entry. Provincial tax and HST treatment can depend on the importer’s registration, the type of goods, the place of supply and whether self-assessment rules apply. An accountant or tax adviser should confirm recoverability and provincial obligations, while the customs entry should follow CBSA requirements.

Other possible charges include:

- Excise duty on specific goods

- Excise tax on designated products

- Anti-dumping and countervailing duties under trade-remedy rules

- Product-specific surtaxes

- Customs broker and disbursement fees

- Examination, storage, demurrage or detention charges

- Permit, inspection or agency fees for regulated goods

Import Duty from China to Canada

There is no single duty rate for all products imported from China. The rate depends on the Canadian tariff classification, country of origin and tariff treatment shown in the current Customs Tariff. Two products with the same supplier value can have very different border costs if their materials, functions or tariff items differ.

Importers should also check whether a product is covered by a current surtax or trade-remedy measure. Certain metals, industrial goods, consumer products or goods from named exporters may be subject to additional duties even when the regular customs tariff rate is low or free.

The shipping country is not always the country of origin. Goods routed through Hong Kong, the United States or another country do not acquire a new origin merely because they were stored, consolidated or transshipped there.

Country of Origin and Tariff Treatment

Country of origin generally refers to where the goods were manufactured, produced or substantially transformed under the applicable origin rules. It is separate from the country of export, supplier location and port of loading.

Origin can affect:

- The tariff treatment and regular duty rate

- Eligibility for preferential treatment under a trade agreement

- Proof-of-origin requirements

- Country-of-origin marking

- Surtaxes and trade-remedy measures

- Import controls or quotas

The commercial invoice should state the origin accurately. When production involves components or processing in several countries, the importer should obtain manufacturing information rather than assuming origin from the supplier’s address.

Customs Value and Value for Duty

Value for duty is the customs valuation base used to calculate duty. It is not always identical to the amount transferred to the supplier or the value printed on a pro forma invoice. In many normal sales for export to Canada, the transaction value method is used, subject to the conditions and adjustments in Canadian customs valuation rules.

Items that may need review include:

- Price paid or payable for the goods

- Assists supplied by the buyer, such as moulds, tooling or design work

- Packing costs and certain commissions

- Royalties or licence fees connected to the imported goods

- Proceeds that revert to the seller

- Transportation and insurance amounts, depending on where the cost is incurred and how the sale is structured

- Currency conversion using the applicable customs exchange rate

Declaring an artificially low value, using a sample value for commercial inventory or omitting assists can lead to reassessment and penalties. Even goods supplied free of charge require an appropriate value for duty.

Do Incoterms Change the HS Code or Duty Rate?

Incoterms allocate transport tasks, costs and risk between the seller and buyer. They do not change the legal classification of the product or create a different customs duty rate. However, EXW, FOB and DDP can affect which party provides documents, pays import charges and controls the freight quotation. They can also affect how cost elements appear on the invoice and therefore what must be reviewed for customs valuation.

For a detailed responsibility comparison, read FOB vs EXW vs DDP for China-to-Canada shipments.

CARM, Business Numbers and Commercial Import Accounts

The CBSA Assessment and Revenue Management system, known as CARM, is used to assess and collect duties and taxes on commercial goods imported into Canada. A commercial importer normally needs a Canadian Business Number and an import-export program account before importing.

Depending on the importer’s operating model, CARM tasks may include:

- Registering the business in the CARM Client Portal

- Delegating access to employees, customs brokers or service providers

- Reviewing customs accounting documents and statements

- Paying duties and taxes

- Managing financial security when using Release Prior to Payment

- Requesting or reviewing rulings and account information

Registration and delegation should be completed before the shipment arrives. The official CBSA CARM portal guidance should be checked for current account and payment requirements.

Documents Needed to Support HS Code, Duty and Tax Review

Classification and customs valuation depend on consistent commercial and technical records. A commercial invoice that only states “accessories,” “parts,” “samples” or “general merchandise” is usually too vague to support a reliable classification.

Prepare the following before booking freight:

- Commercial invoice with seller, buyer, currency, quantity and unit value

- Packing list with carton count, weight and dimensions

- Detailed product description and intended use

- Material composition and technical specifications

- Product photographs, catalogue pages or drawings

- Country-of-origin information

- Supplier’s proposed six-digit HS code, when available

- Bill of lading or air waybill details

- Import permits, certificates or test reports where required

- Importer Business Number and RM account information

For a broader document checklist, review the guide to shipping documents from China to Canada.

Common HS Code, Duty and Tax Mistakes

| Mistake | Why it creates risk | Better approach |

|---|---|---|

| Copying the supplier’s national code | Chinese national digits do not replace the Canadian 10-digit classification | Use supplier information as a starting point and verify the Canadian tariff item |

| Classifying by product name only | Material, function and legal notes may place the product elsewhere | Review specifications, chapter notes and interpretative rules |

| Using one code for a mixed shipment | Different products may have different duty rates and requirements | Classify and value each distinct product line separately |

| Assuming “duty-free” means no border cost | GST, surtaxes, trade remedies and fees may still apply | Calculate all customs and logistics cost components |

| Confusing country of export with origin | Tariff treatment and trade measures may be applied incorrectly | Confirm manufacturing and substantial-transformation details |

| Using an unsupported low declared value | CBSA may reassess the value and apply interest or penalties | Use a defensible customs valuation supported by records |

| Checking the tariff only after departure | Permits, additional duties or product restrictions may be discovered too late | Complete classification and admissibility review before pickup |

| Assuming DDP removes importer compliance | An unclear importer-of-record structure can create tax and customs risk | Confirm the DDP scope, importer of record and supporting documents in writing |

How HS Codes Affect Landed Cost

Landed cost is the total cost of bringing the goods to the final Canadian destination. The HS code affects the customs component, but a reliable landed-cost estimate must include the entire logistics chain.

A complete estimate may include:

- Supplier price

- China pickup and export handling

- International air or sea freight

- Cargo insurance

- Customs duty and GST

- Surtaxes or trade-remedy duties

- Customs brokerage and disbursement fees

- Port, airport or terminal charges

- Storage, demurrage or inspection costs

- Final delivery in Canada

For freight and delivery cost factors, see the guide to shipping costs from China to Canada.

HS Codes and DDP Shipping

DDP means Delivered Duty Paid. It can combine supplier pickup, international freight, import clearance, duties, taxes and final delivery under an agreed service scope. DDP does not make the goods exempt from customs rules, and a responsible provider still needs accurate product descriptions, origin, value and tariff classification.

Before accepting a DDP quotation, confirm:

- Who will act as importer of record

- Which HS code and declared value were used

- Whether regular duty, GST and possible additional duties are included

- Whether the quotation covers customs brokerage and disbursement

- Which products or destinations are excluded

- Whether the importer will receive usable customs and tax records

TopShipping can review whether DDP shipping from China to Canada is practical for the cargo and destination.

How TopShipping Supports Canadian Importers

TopShipping coordinates freight and customs-related information for commercial shipments moving from Chinese suppliers to Canadian destinations. Our role is to help organize the operational data required for quoting, booking and clearance, while binding tariff decisions remain with the CBSA and the importer remains responsible for its customs declarations.

Support may include:

- Collecting product details from the supplier

- Reviewing invoice and packing-list consistency

- Coordinating HS code information with the importer and customs broker

- Planning air freight, sea freight, consolidation or door-to-door delivery

- Identifying missing documents before departure

- Estimating freight and customs-related landed-cost components

- Coordinating cargo release and final delivery in Canada

For shipment-specific import support, review our customs clearance service from China to Canada.

Pre-Shipment HS Code and Import Cost Checklist

- Confirm the exact product name, material, function and model

- Identify the complete 10-digit Canadian tariff classification

- Check the current duty rate and tariff treatment

- Confirm the true country of origin

- Review surtaxes, anti-dumping duties and product restrictions

- Establish a defensible value for duty in Canadian dollars

- Estimate 5% GST and any applicable excise amounts

- Confirm the importer’s Business Number, RM account and CARM access

- Make sure invoice, packing list and transport documents are consistent

- Confirm permits, licences, labels and certificates before pickup

- Document the DDP, FOB or EXW responsibility structure

- Calculate the total landed cost rather than freight alone